Home value? I got your home value right here!

CMAs in the Real Estate Industry

Imagine going to the moon without a rocket or psychedelics.

Now imagine trying to sell or buy a home without knowing its market value. Crazy, right?

To remain grounded and sane, you need a comparative market analysis (CMA), a Realtor’s home value estimate based on recent sales of similar homes.

A real estate agent or broker generates a CMA report to determine a home’s fair market value, which helps a seller set a home’s listing price or a buyer pin down an offer price on a home listing.

The CMA is a critical piece of the home sale puzzle since offering too much for a home or selling for too little could be a costly mistake.

So let’s orbit the CMA analysis to learn about the most efficient way to determine home values.

What Are CMA Basics?

The CMA will provide an estimate of a home’s fair market value given the sale prices of other homes in the area.

When asked for a CMA, a Realtor® will usually research home ownership to confirm that the owner is the one who’s asking.

A Realtor® will compile sales data from the multiple listing service (MLS), an indispensable centralized database of property listings and sales data. The MLS is the source of most real estate data and thus has accurate and up-to-date sales information.

To produce a CMA, a Realtor® will try to find at least three comparable home sales or “comps” that are very similar to the subject property. The sales price of each comp is adjusted for differences in square footage, lot size, age, location, condition, amenities, and anything else that can affect value.

The goal is to find comps that require the least amount of adjustments, which by definition will be most like the subject property.

Depending on the sales, just one or two good comps can be enough to peg the home value, ideally with supporting sales data from inferior comps.

A Realtor will calculate a market value by averaging the adjusted values of all comparable sales or applying more weight to certain comps depending on the degree of similarity.

Making Adjustments to Comps In a CMA

Variety is the spice of life, so thankfully most houses are different. However, that makes CMAs more challenging but nothing that some well-placed adjustments can’t overcome.

It’s the old apples-to-apples routine. By way of dollar adjustments, comparable sales are made similar to the subject property. The adjustments are added to the sale prices to produce “adjusted sale prices.“

In other words, figure out what the comps would sell for in today’s market if they were similar to the subject property.

A Realtor will then reconcile the adjusted sale prices to arrive at an opinion of value. Comps with the least amount of adjustments are usually weighted more heavily. Adjusted prices are multiplied by their relative weight and summed up. For example:

- Comp #1: Adjusted sale price is $325,000 X 40% weight = $130,000

- Comp #2: Adjusted sale price is $340,000 X 30% weight = $102,000

- Comp #3: Adjusted sale price is $345,000 X 30% weight = $103,500

Add the three totals to derive the Adjusted Home Value = $335,500

Some Realtors® will take another step in calculating a price per square foot and applying it to the square footage of the subject property, but it’s unnecessary and can be confusing.

Making detailed adjustments is imperative at the risk of underpricing or overpricing a home, especially in neighborhoods with a wide variety of homes.

Note that value adjustments in CMAs can be subjective. They can rely heavily on a Realtor’s experience with how certain property characteristics will translate into price differences.

What Does a CMA Report Include?

A top-notch Bakersfield Realtor® will include the following home sales information:

Subject and Comps Characteristics

A CMA report will contain a description of the home under consideration, which includes:

- Address

- Location

- Sale Price

- Sale Date

- Living Area (Square Footage)

- Bedrooms

- Bathrooms

- Year Built

- Lot Size

- Garage Type

- Pool (Y/N)

- Upgrades

Location – Proximity of Comps

As we all know, location is paramount in real estate. Included in a CMA report are the addresses of each comparable sale and their respective distances from the subject property. Optimally, comps should be located within the same subdivision or neighborhood. Of course, in rural areas, a Realtor must use whatever comps are available and make the necessary adjustments.

Other location considerations include whether the home is adjacent to a busy road, sits in a cul-de-sac, sits on a corner lot, or two-story neighbors can see into your backyard.

Sale Status

Comparable home sales fall into one of the following statuses:

- Sold – Homes that have closed escrow, which are the most relevant comps depending on recency.

- Pending – Homes that are under contract (in escrow). They can be highly relevant comps providing they close escrow and are supported by sold comps.

- Active – Homes that are listed for sale and not yet under contract. They are the least relevant comps since prices can change and listings can be canceled.

Sale Date

The more recent the sale, the better the comp. Usually, comps that have been sold within a few months should be used, but some CMAs will require going further back in time. In that situation, value adjustments should be made depending on whether the market is rising or dropping. For example, a 6-month-old comp might require a 5% upward adjustment if the market is increasing at a 10% annual rate.

Square Footage

The square footage of the living space is included for the subject property and each comparable sale. The size of garages, outdoor patios, and unfinished basements are typically not included. Adjustments are applied to size differences from $40-$100/square foot, based on local construction costs and the subject’s building quality.

Bedrooms and Bathrooms

Ideally, the subject property and all comps should have the same number of bedrooms and bathrooms. When that’s not possible, adjustments can be made for any disparity.

Note the importance to avoid making double adjustments for an extra bed or bath in addition to an adjustment for square footage.

For example, let’s say the subject property has 3 bedrooms and 1,800 square feet; and a comp has 4 bedrooms and 2,100 square feet. At $50/sq ft, the 300 square feet difference would equate to a $15,000 adjustment. An additional adjustment for the extra bedroom would be double-counting the square footage difference, so may not be warranted.

On the other hand, two homes of the same size might have 3 bedrooms and 4 bedrooms respectively. There’s no adjustment for square footage, but a local Realtor should have a good feel for whether an extra bedroom will warrant an adjustment. Is an extra bedroom worth more even though the bedrooms are smaller?

Year Built

It may seem obvious but a home’s age and the comps’ ages should be as close as possible. Generally, ages within a 5-10 year range may not warrant adjustments. Homes’ ages that are 50 years apart would clearly warrant a value adjustment – or perhaps there’s a better comp available. A good Bakersfield Realtor would be able to make a judgment call about those adjustments.

Lot Size

Making value adjustments for lot size can be tricky. Appraisers typically follow accepted adjustment guidelines for a particular area, but those don’t necessarily reflect the reality of buyer demand.

In most neighborhoods, a 10,000-square-foot lot will command a premium over a 7,500-square-foot lot. Which lot would better accommodate a pool, a shed, or extra decking? The exact value adjustment is debatable but appraisers will often not adjust at all.

RV Parking

In the Bakersfield market, a premium is placed on a lot with RV parking that’s the same size as another lot without RV parking. The value adjustment can be subjective but $5,000 – $10,000 would be reasonable if you compare the cost of renting an RV storage space for a few years at $75 to $200 per month with much less convenience.

Garage or Parking

In the age of too much stuff, a 3-car garage can command an estimated value adjustment of $5,000-$10,000 over a 2-car garage.

Pool

In Bakersfield or any market with hot summers, a premium is placed on the cool sensation of an inviting oasis. Adjustments can range from $15,000 to $50,000 depending on the size of the pool and related hardscaping.

It’s readily reported that the cost of installing a pool does not add equivalent value. That’s true, but many Realtors believe that more cost would be recouped in hot weather markets if appraisers were given more latitude with value adjustments.

Solar Equipment

Many Bakersfield homes have solar systems to help minimize monthly electric bills, which are absurd and getting worse. However, not all solar systems are created equal. Some systems are owned outright while others are being purchased with financing. Some are leased while others are under Power Purchase Agreements (PPA).

The only solar systems that add value are owned outright. Depending on the size of the system, adjustments can range from $10,000 to $20,000.

Condition

There are classifications of construction quality or condition at most county assessor’s offices, but those are not always accurate. By visible inspection or even a close look at photos, a Realtor can often determine whether value adjustments should be made.

Upgrades

Like the property’s condition, value adjustments can be made for upgrades to the subject property relative to comparable properties. Value-added improvements include kitchen, bathroom, or flooring upgrades; shops, stables, or anything on which a buyer would place a premium.

It’s worth repeating that a Realtor® makes value adjustments in a CMA report to support a realistic listing price for a home sale, while an appraiser is usually appraising a home after a home is already under contract.

See a separate blog post for upgrades that may not add value.

Market Condition Repetition

As mentioned before, market conditions set the stage for an accurate CMA. Comparable sales should be used that have sold close to the valuation date or a rapidly changing market will compromise accuracy.

In a rapidly appreciating neighborhood, a comp that’s just a few months old could be thousands of dollars under market value. Fortunately, sales volume typically increases in a rising market so there should be plenty of recent comps available. If that’s not the case then the appropriate adjustments must be made.

On a side note, appraised values might not keep pace with rapidly rising market values. Often, sellers and buyers will agree on price, but buyers are forced to contribute more cash to cover appraisal gaps. This isn’t an issue in a flat or declining market.

Seller Concessions

A comparable sale should be adjusted down for any seller concessions, like any buyer’s closing costs paid by the seller. Bakersfield Realtors® have access to this information from the MLS.

Often included in seller concessions are the cost of repairs that the seller agrees should be made, but does not want the hassle of arranging. Instead, the seller pays the equivalent amount of closing costs for the buyer.

The above-mentioned cost of repairs can often include major expenses like a new HVAC system or a new roof. In these cases, home improvements don’t necessarily add value because most buyers will expect functioning mechanicals and a roof that doesn’t leak. Instead, a home’s value is penalized when those improvements are not made.

To See Or Not To See

A Bakersfield Realtor will typically visit a home before working up a CMA. A good Realtor® will take notes about anything worthy of mentioning as a positive or negative, whether interior or exterior.

Most small items will not have any impact on the home’s value but the Realtor can use that information to complete a listing marketing description and the requisite AVID form (Agent’s Visual Inspection Disclosure).

A Realtor can sometimes be asked for a CMA by a homeowner who is not yet ready to sell.

In this situation, it’s not always necessary to visit the property to provide an accurate CMA, which can still be derived by viewing photos and discussing the property with the owner.

A CMA Example

See below for a CMA in action! A Bakersfield couple wants to sell their home, so a CMA was generated to set a listing price.

Home Details:

- The house is 2,175 square feet with 4 bedrooms and 2 bathrooms.

- The lot is 7,500 square feet on a street that’s not adjacent to any busy roads.

- The house was built in 2005. Kitchen cabinets, counters, and appliances were upgraded.

Comparable Sales Details:

- 4 comps were used, but three would suffice depending on similarity.

- 4 comps sold within two months of the CMA report, so no adjustments were made for time.

- 3 comps were close to the subject in size (within 200 sq ft), so no adjustments were made.

- 1 comp was 220 square feet larger so a $50/sq ft adjustment was made, or $11,000.

- 2 comps were adjusted $5,000 for lot size differences.

- For several comps, other adjustments were made for lot size, garage, and pool.

- The subject property and all comps had upgrades, so no adjustments were made.

In this CMA, the average adjusted value of all comps is $407,000.

Normally, Comp #1 would be weighted more heavily than the others but all the adjusted values are in a tight range. Even weighting Comp #1 at 100% equates to $405,000 which is very close to $407,000.

In a flat market, a competitive list price would be $409,000.

In a rising market, a list price of $419,000 might be advisable.

[wpdatatable id=3]

It’s important to reiterate that CMA value adjustments can be subjective. They can rely heavily on a Realtor’s experience with respect to how certain property characteristics will translate into price differences.

Build Your Own CMA Report – DIY Fun!

You too can create a CMA report by tapping into any of the common real estate websites. Keep in mind that a Bakersfield Realtor will typically provide a CMA for free and without obligation, but you may want to get a handle on your home’s value ahead of time.

Let’s take a quick look at using Redfin to gather the necessary data to complete your very own comparative market analysis.

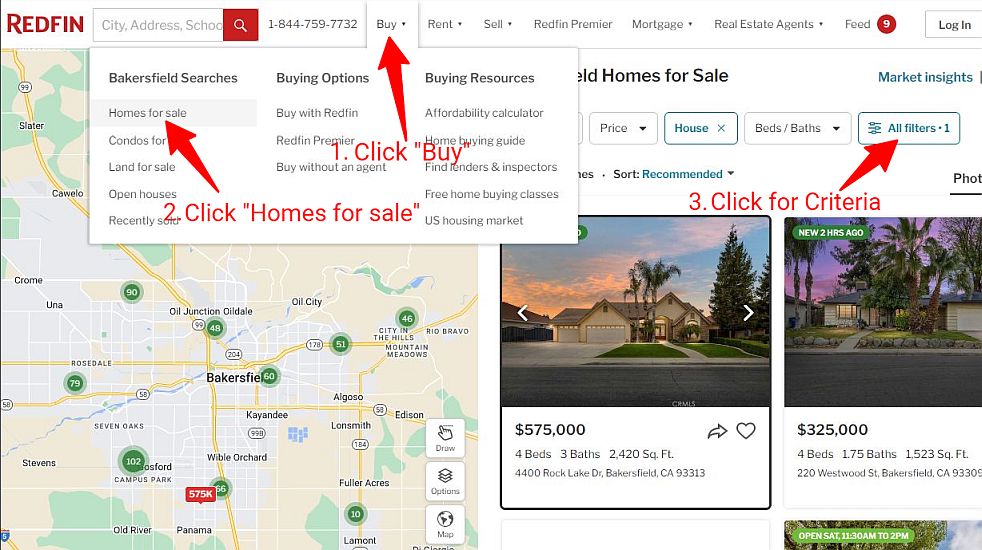

First, start by finding your city. Just input your city into the main search box.

Then click “Buy.” Then click “Homes for sale.”

Then click “All filters” to access all other criteria.

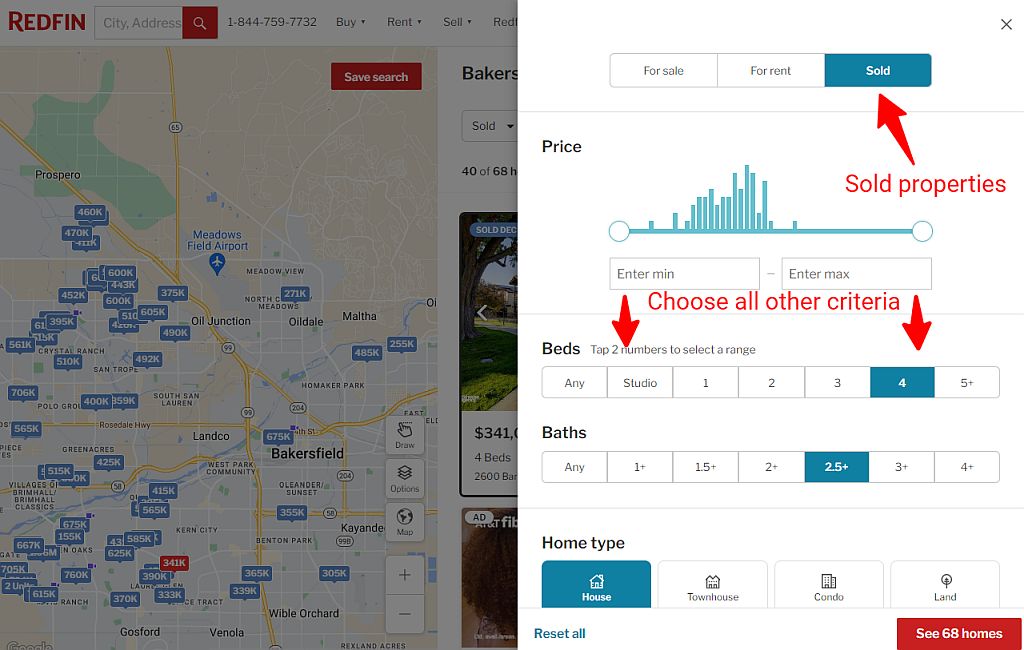

Then choose the property search criteria. Only use SOLD properties for highest accuracy.

Start with the same number of bedrooms and bathrooms, then bracket the square footage by 300 square feet, both higher and lower than your property.

Zoom in on your neighborhood and choose the best comps according to location.

Expand the search criteria and/or the search radius if you can’t find enough comps.

CMA vs. Appraisal

A CMA is a free and quick home valuation done by a Realtor®, usually for a client.

An appraisal is a formal report done by a licensed appraiser, usually for a lender.

An appraisal typically costs between $350-$500 but can run higher for larger homes, multi-family, or commercial properties.

An appraisal typically takes one to three weeks to complete, depending on the appraiser’s workload and whether a buyer pays extra for a rush job.

For an appraisal, an appraiser generates a detailed report comparing a subject property to recent sales of similar homes. Like a CMA, price adjustments are made in a grid-type format that lists differences in property size, age, location, condition, and amenities.

Photos of the subject property and comps are typically included for the lender.

CMAs are not regulated or standardized and can often be condensed into one page.

CMA vs. Broker Price Opinion

A comparative market analysis (CMA) and a broker price opinion (BPO) are similar, but there are differences.

Both CMAs and BPOs are home valuation reports generated by real estate agents or brokers. A home seller can use a BPO to determine an accurate listing price while buyers can use a BPO to determine a competitive offer on a home listing.

However, mortgage lenders and real estate asset managers usually request BPOs, while Realtors provide CMAs to potential home sellers and buyers.

BPOs provide quick and cost-effective value estimates of properties that secure troubled loans and foreclosed properties (also known as “real estate owned,” or REO properties).

Also, a BPO usually costs between $50 to $250 for lenders. A Realtor will provide a free BPO to a potential client but may charge a fee if a seller is trying a for-sale-by-owner.

CMA vs. Automated Valuation Models (AVM)

An automated valuation model (AVM), or a home value estimator, is a computer algorithm that compares a home to recent home sales to estimate its value.

The AVM pulls publicly available property data like sale price, sale date, type, size, age, and the proximity of the sales comps. The algorithm crunches all those variables to provide an immediate value estimate.

For now, humans perform home value estimates more accurately than computers. An AVM cannot accurately judge differences in condition, upgrades, slight differences in location, and other nuances. However, computers may take over when numerical values can be assigned to somewhat subjective characteristics.

AVMs are handy for a quick ballpark estimate of a home’s value, but they are not adequate substitutes for CMAs in setting listing prices.

[wpdatatable id=4]

A Bakersfield Realtor’s Comparable Market Analysis (CMA)

For a free and accurate estimate of a home’s value, get a CMA report from a top Bakersfield Realtor.

Bakersfield Realtors® are plugged into real-time sales data and current market conditions. Homebuyers and sellers can nail down the current market values of a homes. From that knowledge, they can feel confident about making their move and maybe even the future of the universe.

Related Articles

What’s an Automated Valuation Model (AVM)?

What’s a Broker’s Price Opinion?

Pricing a Home For Sale: Don’t Make This Huge Mistake

What Do Appraisers Value Most?